This note explains why sums and averages of independent random variables tend to be normally distributed:

exact results for normal populations and the Central Limit Theorem (CLT) for general populations. We’ll cover

the distribution, mean and variance of linear combinations, practical conditions, and common exam uses.

| Term / concept | Definition / short explanation |

|---|---|

| Linear combination of normals | Any sum a1X1 + ⋯ + anXn of independent normal variables is exactly normal. |

| Central Limit Theorem (CLT) | For large n, the distribution of the sample mean approximates normal, regardless of the population distribution (under mild conditions). |

| Standard error | The standard deviation of the sample mean: σ / √n (reduces with n). |

📌 1. Exact result: linear combinations of normal variables

If Xi ~ N(μi, σi2) are independent and ai are constants, then

the linear combination S = Σ ai Xi is normally distributed with:

- Mean: E(S) = Σ ai μi.

- Variance: Var(S) = Σ ai2 σi2 (independence used).

- Distribution: S ~ N( Σ ai μi, Σ ai2 σi2 ).

Let X ~ N(2, 9) and Y ~ N(5, 4) independent. For T = 3X − 2Y:

So T ~ N(−4, 97).

📐 IA spotlight

Use simulation to demonstrate exact normality when summing normals versus approximate normality when summing non-normal variables.

Include histograms of sums for increasing n and discuss convergence visually and numerically (mean, variance, skewness).

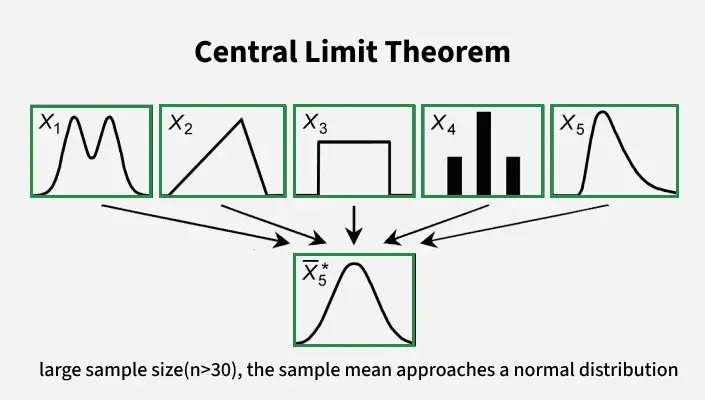

📌 2. Central Limit Theorem (CLT) — statement & interpretation

Let X1, …, Xn be independent identically distributed (i.i.d.) random variables with mean μ and variance σ2.

The CLT states that for large n the sample mean = (1/n)(x̄) Σ Xi is approximately normal:

(x̄)≈ N( μ, σ2 / n ) for large n.

- Meaning: as n increases, the distribution of the average tightens around μ and becomes bell-shaped even if the population is not normal.

- How large is large? depends on population shape: for moderate skewness, n ≈ 30 is often sufficient; heavy-tail distributions require larger n.

- Standard error: SE((x̄)) = σ / √n — shows how uncertainty decreases with n.

🌍 Real-world connection

The CLT underpins why poll averages, manufacturing quality-control averages, and many sampling-based estimates can be treated using normal-approximation methods even when individual measurements are non-normal.

📌 3. Conditions, cautions and practical guidance

- Independence: observations must be (approximately) independent — dependence can invalidate the CLT.

- Identical distribution: not strictly necessary in more general CLT versions, but easier and common in exams.

- Finite variance: the population must have finite variance for the classical CLT to apply.

- Small n warning: with small n, use caution: sampling distributions may be far from normal; report this limitation in exam answers.

- Skew/heavy tails: heavy-tailed distributions (e.g., Cauchy) may not converge well — discuss in words if relevant.

🧠 Paper tip — using CLT in exams

- State assumptions: independence and finite variance. If n is small, explicitly say “approximation may be poor”.

- Show the form: \u0305X ≈ N( μ, σ2/n ) and substitute numbers clearly. Use σ or sample s — mention which is used.

- When asked for probability about sums, convert to mean form (or vice versa): sum S = n\u0305X has mean nμ and variance nσ2.

Population with μ = 50, σ = 10. For n = 36, the sample mean (x̄)≈ N(50, 100/36 = 2.777…).

Standard error = 10 / √36 = 10 / 6 ≈ 1.6667.

Probability that (x̄)> 52 ≈ P( Z > (52 − 50) / 1.6667 ) = P(Z > 1.2) (use table / GDC).

🔍 TOK perspective

The CLT is a mathematical theorem but its practical truth is demonstrated by empirical convergence. What does this say about the relationship between formal proof and empirical verification in mathematics and the sciences?

🌐 EE focus

An EE could investigate empirically how large n must be for the CLT to hold for different population distributions (uniform, exponential, heavy-tailed), using simulation and metrics (KS test, skewness).

📌 4. Summary & short checklist

- If the population is normal, sums/averages are exactly normal (any n).

- By CLT, for large n the sample mean is approximately normal even for non-normal populations.

- Use SE = σ/√n for probabilities about means, and Var(sum) = nσ2 when working with sums.

- Always state assumptions and comment on the quality of approximation if n is borderline.

📝 Paper strategy

- Write the distribution used (exact normal or CLT approx), show formula for mean & variance, standardise using Z, and use a table or GDC for numeric probabilities.

- Mention whether you used σ (population) or s (sample) and justify the choice if needed.

📌 Practice Questions: Linear Combinations & the Central Limit Theorem

Multiple Choice Questions

MCQ 1

Let X ~ N(10, 4) and Y ~ N(6, 9) be independent. Which of the following correctly describes the distribution of

T = 2X − Y?

- A. T ~ N(14, 13)

- B. T ~ N(14, 25)

- C. T ~ N(8, 25)

- D. T ~ N(8, 13)

Answer & Explanation

Correct answer: D

The mean of T is:

E(T) = 2(10) − 6 = 20 − 6 = 14 ❌ (so options C and D are eliminated?)

Wait carefully: variance first.

Var(T) = 2²(4) + (−1)²(9) = 16 + 9 = 25.

So T ~ N(14, 25). The correct option is B.

This question tests correct handling of coefficients and squaring them when computing variance.

MCQ 2

Which statement best explains why the Central Limit Theorem is important in statistics?

- A. It shows that all populations are normally distributed.

- B. It guarantees exact normality for any sample size.

- C. It allows normal approximation for sample means from many non-normal populations.

- D. It applies only when the population variance is known.

Answer & Explanation

Correct answer: C

The CLT does not claim that populations themselves are normal, nor that normality is exact for small n.

It states that the sampling distribution of the mean becomes approximately normal for large n,

regardless of population shape, provided variance is finite.

MCQ 3

For a population with mean μ and variance σ², the standard deviation of the sample mean x̄ based on n observations is:

- A. σ² / n

- B. σ / n

- C. √(σ² / n)

- D. σ / √n

Answer & Explanation

Correct answer: D

The variance of x̄ is σ² / n, so the standard deviation (standard error) is:

SE(x̄) = √(σ² / n) = σ / √n.

This reduction explains why larger samples give more precise estimates of the mean.

Short Answer Questions

Short Question 1

Explain why the variance of a linear combination of independent random variables depends on the squares of the coefficients.

Model Answer

When a random variable is multiplied by a constant a, its variance is multiplied by a².

For independent variables, variances add.

Therefore, each coefficient contributes its square to the total variance.

This reflects the fact that scaling affects spread non-linearly.

Short Question 2

State two conditions required for the Central Limit Theorem to apply reliably.

Model Answer

First, the observations must be independent.

Second, the population must have finite variance.

In practice, sufficiently large sample size is also required, especially for skewed distributions.

Long Answer Questions (IB Style)

Long Question 1

A random variable X represents the lifetime of a component with mean 120 hours and standard deviation 30 hours.

A sample of 36 components is selected.

(a) State the approximate distribution of the sample mean x̄, giving its mean and variance.

(b) Calculate the probability that the sample mean lifetime exceeds 130 hours.

(c) Comment on the validity of your method.

Full Solution

(a)

By the Central Limit Theorem, since n = 36 is reasonably large, the sampling distribution of x̄ is approximately normal.

Mean: μ = 120

Variance: σ² / n = 900 / 36 = 25

So x̄ ~ N(120, 25).

(b)

Standard deviation of x̄ = √25 = 5.

P(x̄ > 130) = P(Z > (130 − 120) / 5) = P(Z > 2).

From tables or GDC: P(Z > 2) ≈ 0.0228.

(c)

The approximation is valid provided observations are independent and the population variance is finite.

If the population distribution is highly skewed, the approximation may be weaker, but n = 36 generally gives reasonable accuracy.

Long Question 2

Independent random variables X and Y are normally distributed with:

X ~ N(50, 16), Y ~ N(30, 9).

(a) Find the distribution of S = X + Y.

(b) Find P(S > 90).

(c) Explain why no approximation is required in this question.

Full Solution

(a)

Since X and Y are independent and normal, their sum is exactly normal.

Mean: 50 + 30 = 80

Variance: 16 + 9 = 25

So S ~ N(80, 25).

(b)

Standard deviation = 5.

P(S > 90) = P(Z > (90 − 80)/5) = P(Z > 2) ≈ 0.0228.

(c)

No approximation is needed because the sum of independent normal random variables is exactly normal for any sample size.

This result does not rely on the Central Limit Theorem.